A Rebound In Stocks And A Pivot For Bonds

Now that we are halfway through 2023, it is a good time to reflect on the year’s first six months and identify opportunities available to our clients. The rebound in equities so far this year has been led by developed markets around the globe, with the S&P 500 (U.S. large-cap stocks) entering a new bull market, or an increase of at least 20% from its October 2022 low, along the way. U.S. small-mid cap and international stocks are up 9-10% year-to-date. But the good news doesn’t stop with equities. Total returns for bonds are also positive so far this year. The big story in fixed income is the switch from price appreciation to income as the main return driver. Also, as we get closer to the end of the Federal Reserve’s rate hikes to fight inflation, our clients have new opportunities to take advantage of more income and higher return potential, especially in bonds.

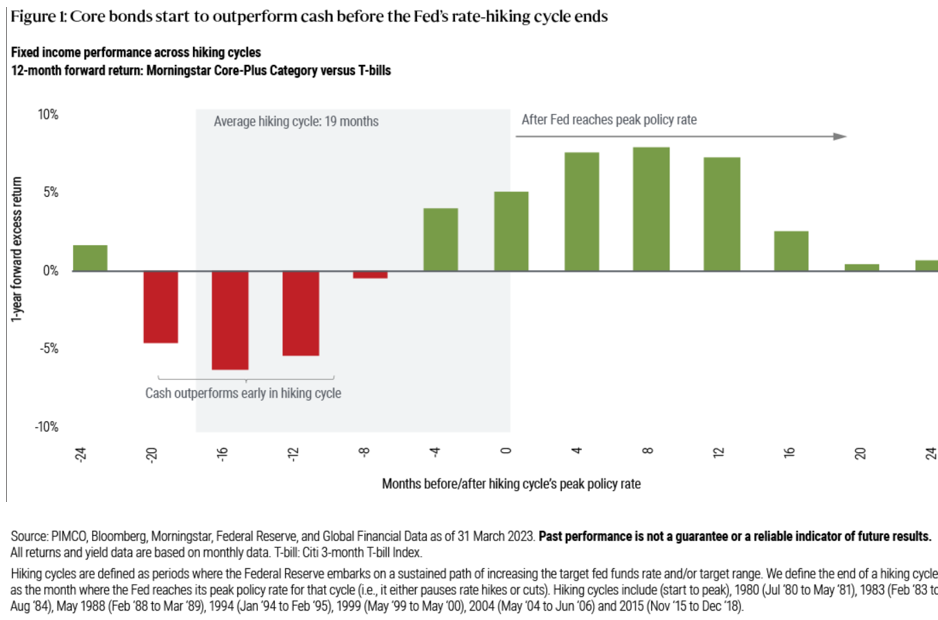

Since the Fed started raising interest rates last year, clients who have been wary of market volatility or want to park cash for upcoming spending needs have found higher rates in money market funds and bank CDs. We have helped many clients utilize TD Ameritrade/Schwab’s money market mutual funds for those purposes, and we believe they are still appropriate for short-term spending needs. However, it won’t be easy for clients who consider their money market funds as investments to maintain those higher short-term rates as longer-term rates begin to increase and eventually normalize. Also, many market analysts expect the Fed to cut rates in 2024 to counter any recession. The intermediate-term, investment-grade, taxable U.S. Core Plus bond fund in our clients’ portfolios has increased its average bond maturity. The managers feel that now is a good opportunity to focus on longer-maturity fixed income. While the Fed could still raise rates higher, the current higher yields can provide a buffer against these increases. Research has shown that the time to shift cash into core fixed income is as the Fed approaches its peak policy rate (i.e., before it pauses or cuts). Please see Figure 1 below, courtesy of PIMCO:

Over the typical 19-month hiking cycle, rates initially rise and cash (3-month Treasury bills) outperforms Core Plus fixed income. This occurred in 2022 when bonds had a negative return from the Fed’s aggressive rate increases. However, before the Fed reaches its peak policy rate, Core Plus fixed income allocations begin outperforming cash. As always, we are here for you if you have any questions.