Now that we are halfway through 2023, it is a good time to reflect on the year’s first six months and identify opportunities available to our clients. The rebound in equities so far this year has been led by developed markets around the globe, with the S&P 500 (U.S. large-cap stocks) entering a new bull market, or an increase of at least 20% from its October 2022 low, along the way. U.S. small-mid cap and international stocks are up 9-10% year-to-date. But the good news doesn’t stop with equities. Total returns for bonds are also positive so far this year. The big story in fixed income is the switch from price appreciation to income as the main return driver. Also, as we get closer to the end of the Federal Reserve’s rate hikes to fight inflation, our clients have new opportunities to take advantage of more income and higher return potential, especially in bonds.

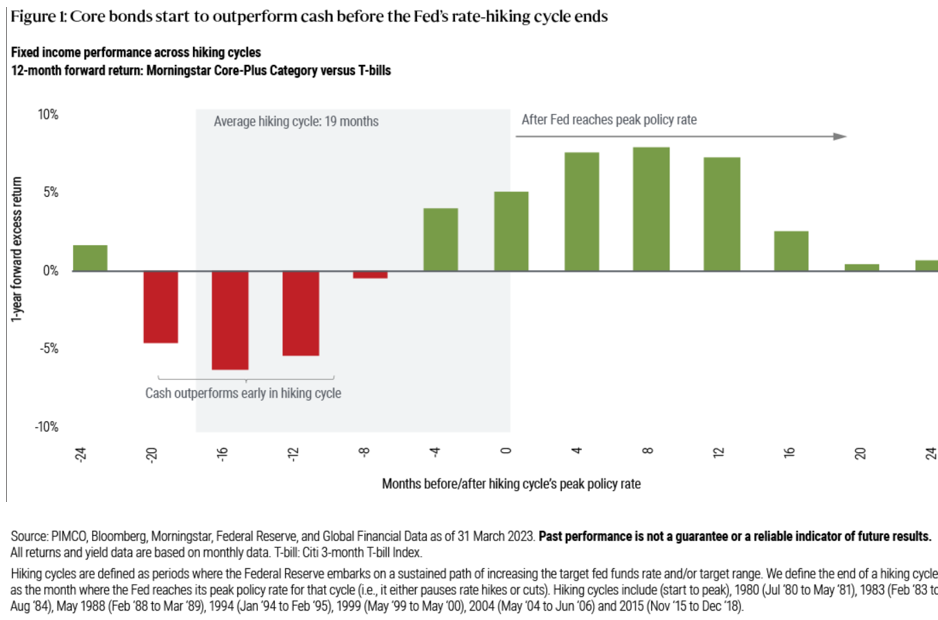

Since the Fed started raising interest rates last year, clients who have been wary of market volatility or want to park cash for upcoming spending needs have found higher rates in money market funds and bank CDs. We have helped many clients utilize TD Ameritrade/Schwab’s money market mutual funds for those purposes, and we believe they are still appropriate for short-term spending needs. However, it won’t be easy for clients who consider their money market funds as investments to maintain those higher short-term rates as longer-term rates begin to increase and eventually normalize. Also, many market analysts expect the Fed to cut rates in 2024 to counter any recession. The intermediate-term, investment-grade, taxable U.S. Core Plus bond fund in our clients’ portfolios has increased its average bond maturity. The managers feel that now is a good opportunity to focus on longer-maturity fixed income. While the Fed could still raise rates higher, the current higher yields can provide a buffer against these increases. Research has shown that the time to shift cash into core fixed income is as the Fed approaches its peak policy rate (i.e., before it pauses or cuts). Please see Figure 1 below, courtesy of PIMCO:

Over the typical 19-month hiking cycle, rates initially rise and cash (3-month Treasury bills) outperforms Core Plus fixed income. This occurred in 2022 when bonds had a negative return from the Fed’s aggressive rate increases. However, before the Fed reaches its peak policy rate, Core Plus fixed income allocations begin outperforming cash. As always, we are here for you if you have any questions.

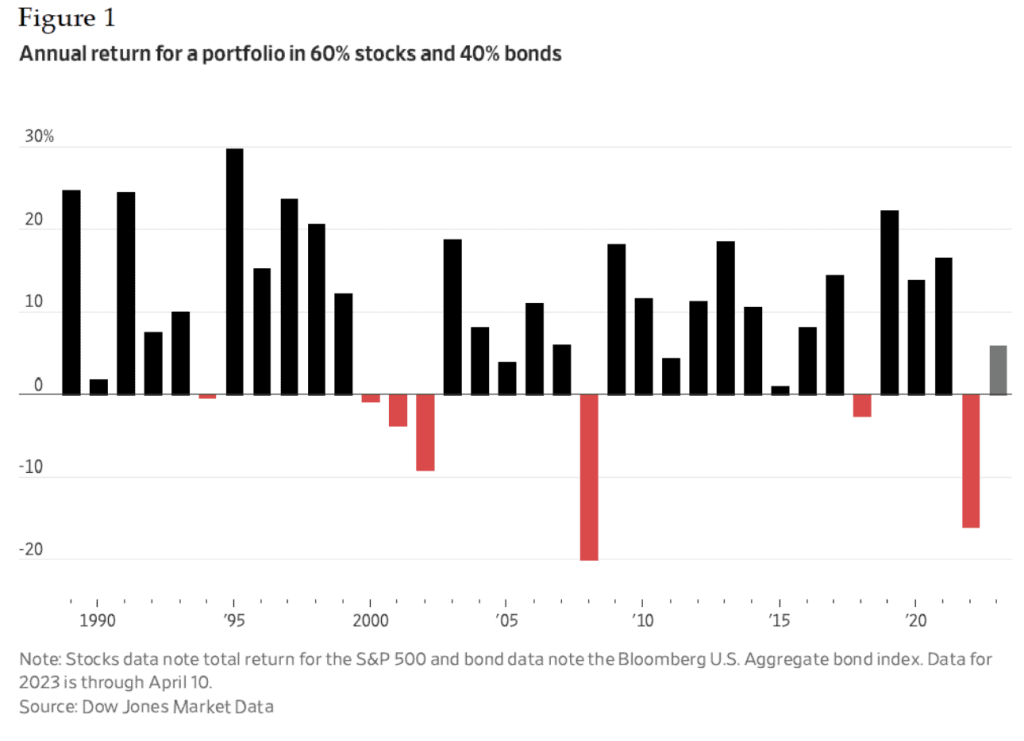

The 60-40 investment strategy has rebounded so far in 2023

The 60-40 portfolio, which is generally described as a portfolio made up of 60% U.S. large-cap stocks (S&P 500) and 40% U.S. core taxable bonds (Bloomberg U.S. Aggregate), is considered the classic investment strategy in the wealth management industry. It is based on the theory that over the long term, diversification among different asset classes should smooth out portfolio returns. For example, bonds can help mitigate downturns in equities, while equity investors who “buy the dip” during those downturns are rewarded in any subsequent upturn. The 60-40 portfolio was down 16% in 2022 as both bonds and stocks were negative (an infrequent occurrence), leading some naysayers to predict its demise. However, the Wall Street Journal did an analysis of annual returns for that portfolio over the past 35 years (Figure 1), and the portfolio was mostly positive, averaging an annual return of 9.3% since 1988.

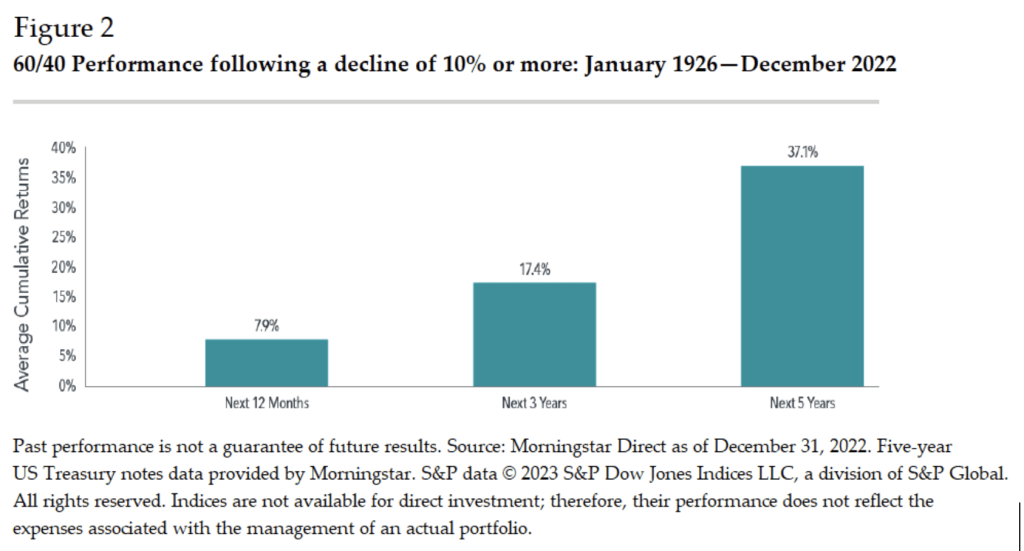

There is also reason to be optimistic about the prospects of the 60-40 portfolio going forward. So far this year, it is up over 5% through early April. While this is a very short time, Dimensional Fund Advisors produced the chart in Figure 2 that shows the 60-40 average cumulative returns (using 5-year U.S. Treasuries for bonds) following a decline of 10% or more.

There are a couple of differences between this traditional view of a 60-40 portfolio and BFA’s corresponding portfolio, but the outlook is the same if not better. First, our 63-37 portfolio uses more than just U.S. large-cap stocks and U.S. core bonds. We also utilize U.S. small- and mid-cap stocks, Foreign developed and emerging stocks, U.S. REITs (real estate), tax-exempt bonds, and international bonds. Second, unlike our client portfolios, no wealth management fees are applied to the 60-40 returns shown here. We believe we can outperform even taking fees into account. The BFA “Core Plus” investment process provides ample opportunities for outperformance and we are confident in the portfolio’s future.

Financial Planning Concepts

UNFORTUNATE ESTATE PLANNING MISTAKES IN WEALTHY FAMILIES

In 2002, Harvard University published a book by their then Senior Philanthropic Adviser, Charles W. Collier, called Wealth in Families. It contains several important considerations for passing wealth through generations of families.

“Shirtsleeves to Shirtsleeves in Three Generations”: Missing Purpose

Our first goal in the wealth transfer process should be to support the next generation by helping them discover a calling that will enhance their personal fulfillment and happiness through work. Collier quotes Jay Hughes, Jr., author of Family Wealth: Keeping It in the Family, as saying “In every culture that I’ve encountered – in China, Latin America, and Europe, for example – I run into the same proverb… The proverb means that the first generation makes the money, the second generation preserves it, the third generation spends it, and the fourth generation must re-create it.” According to Hughes, without the experience of work, the third and fourth generations dissipate the wealth because they lose the incentive to work. He says, “Work in its deepest dimension equates to a calling. Discovering your calling is the most important task an individual can undertake”.

Lack of Communication

A second fundamental goal in the transfer of wealth should be more communication. Collier says, “People are often secretive about family wealth.” Of course, the silence breeds mistrust and misinformation and a lot of time and energy is spent by the family trying to find out the secrets! “More communication is almost always better. Talking to your children early about the meaning and purpose of your family wealth can also enhance your relationship with your children.” The larger the estate, the more significant the importance of discussing your family’s greater vision for the wealth while you are still here. To add purpose, philanthropy should be a critical part of this discussion.

Lack of Experience

Finally, Collier recommends providing the next generation with a pre-inheritance experience. It is a common refrain among wealthy families where the first generation intends to pass the accumulated wealth but they never prepare the children for receiving the wealth. It is a bit like inheriting a football and the next day being expected to start as quarterback for the Green Bay Packers! It doesn’t go well. “They need the freedom to take risks, to make mistakes, and, often, to fail. One approach is to give them a modest amount of money outright at age 21, or 25, monitor their progress, and then give them the balance of the financial inheritance around 35 to 40, often in trust.” Robert Coles, author of Privileged Ones: The Well-Off and Rich in America, takes it one step further by saying, “I feel strongly that parents should not give their children a significant financial inheritance during their career-building years, say ages 22 to 35.” He thinks they shouldn’t receive most until around age 40. “They need to make it on their own if they’re going to achieve any kind of competence,” he said. When combined with an individual purpose and family communication, a little experience can go a long way.